Last week I finally initiated a position in Simon Property Group (SPG). I’ve been watching this high-quality REIT closely but preferred to buy stocks of other companies during the last two years. Finally, it all came together: money burning in my pocket and pressure on SPG’s stock price which resulted in a high dividend yield and a compellingly attractive valuation. I think this is one of the only few low-risk, high-yield investment opportunities at the moment as the U.S. stock market continues to hit all-time highs.

The Business Sector

Sometimes a whole business sector faces challenges whether it’s a compliance issue, technological developments or fundamental questions about the business model. Some think this is the case with traditional retail. I don’t think a retail apocalypse is at hand and fears are overblown. Some REIT’s will just have a difficult time with struggling or bankrupt tenants and may cut their dividend because of a declining occupancy rate and their (increasing) debt load.

Why SPG Stands Out From The Rest

In their 2018 annual report we can read about their astounishing accomplishments:

“Through disciplined execution, our strategy has resulted in industry-leading results, year in and year out. Our Company has achieved growth and scale that few could have imagined possible and the following are just some of the impressive numbers to report over the last 25 years:

• Our annual funds from operations (“FFO”), an important industry measure, has grown from $150 million at the time of our IPO to more than $4.3 billion in 2018.

• We have increased the Company’s annual FFO generation by more than twenty- five times since our IPO.

• Total consolidated revenue has increased more than thirteen times from $424 million to approximately $5.7 billion.

• The gross market value of our portfolio has increased from $3.5 billion to more than $90 billion.

• From our IPO through year- end 2018, ownership of Simon Property Group (SPG) common stock provided a total return to shareholders of more than 2,750%, or a compound annual return of more than 14% compared to the S&P 500 compound annual return of 9% over the same period.”

Past results and averages are not the same as what the company will earn on the next dollar of capital it puts into the business. But it can be used as a guide especially for high-quality businesses or businesses run by high-quality management. Therefor I’m not too worried about the challenges of SPG. They’re able to gradually refinance their debt whether a recession sets in or not. And at low interest rates, because SPG is a S&P 500 A-rated company. They also have a very strong balance sheet with $7 billion in low-cost liquidity and $1.5 billion in retained cash flow. This gives SPG the ability to continuously invest in and improve their real estate portfolio, repay their debt, increase their dividend or even buyback shares. I believe the stock price has significantly come down without any real news with respect to the underlying business.

The Transaction

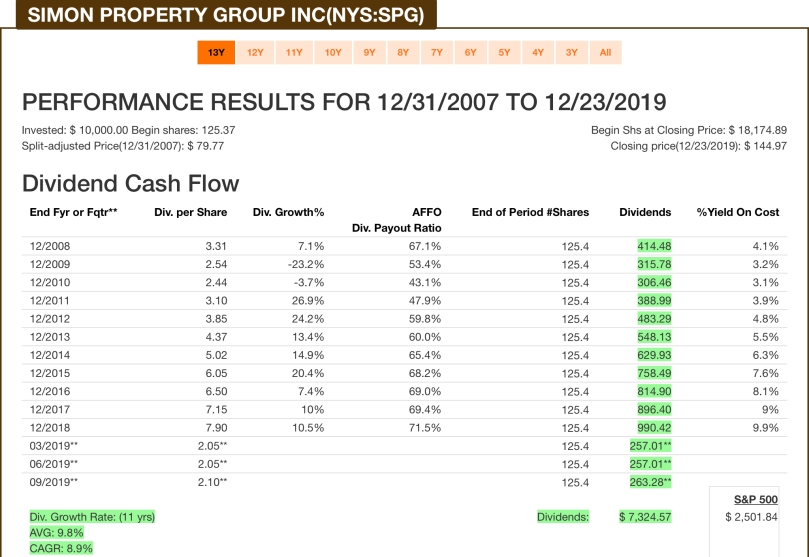

I bought 20 pieces of SPG at a price of $145.98. This means a P/AFFO slightly above 13. Their normal P/AFFO Ratio over 10 and 5 years is more or less 19. So I’m good on the valuation side. With purchasing SPG at this price I get a dividend yield of 5.75%. Their latest dividend raise was a small 2.4% from $2.05 to $2.10. SPG tends to increase their dividend twice a year.

Their longer term dividend growth rate averages out to 10%. That’s very impressive! Their AFFO dividend payout ratio has only slightly increased from 67% to 72% over that same time frame. We can therefor conclude that the dividend is safely covered with funds from operations. During the Great Recession SPG lowered its dividend in 2009 and 2010 though. But over the last 10 years they’ve already managed to acquire the status of a Dividend Contender again. This shows what a quality business this is.

There’s a fascinating text in the 2018 annual report of SPG about their dividend history. “We have paid more than $28 billion in dividends over our 25-year history as a public company, and at our current dividend rate, by the second quarter of 2019, we will have cumulatively paid more than $100.00 per share in dividends since our IPO. Especially considering that our IPO price was $22.25 per share—WOW!” That just sums it all up: WOW!

SPG is a high-quality REIT with a dividend yield of 5.75%, a payout ratio of 72% and a fortress-like balance sheet. With this buy I added $42 to my quarterly dividend income, which totals up to a FY $168. I’m very content with this new position. What’s not to like?

What did you buy lately? Please feel free to comment.

Happy investing!